Agility has become an important initiative for many organisations as they struggle to cope with the...

The Art of Balance: Between Precise Planning and Agile Business Management

December 17, 2024

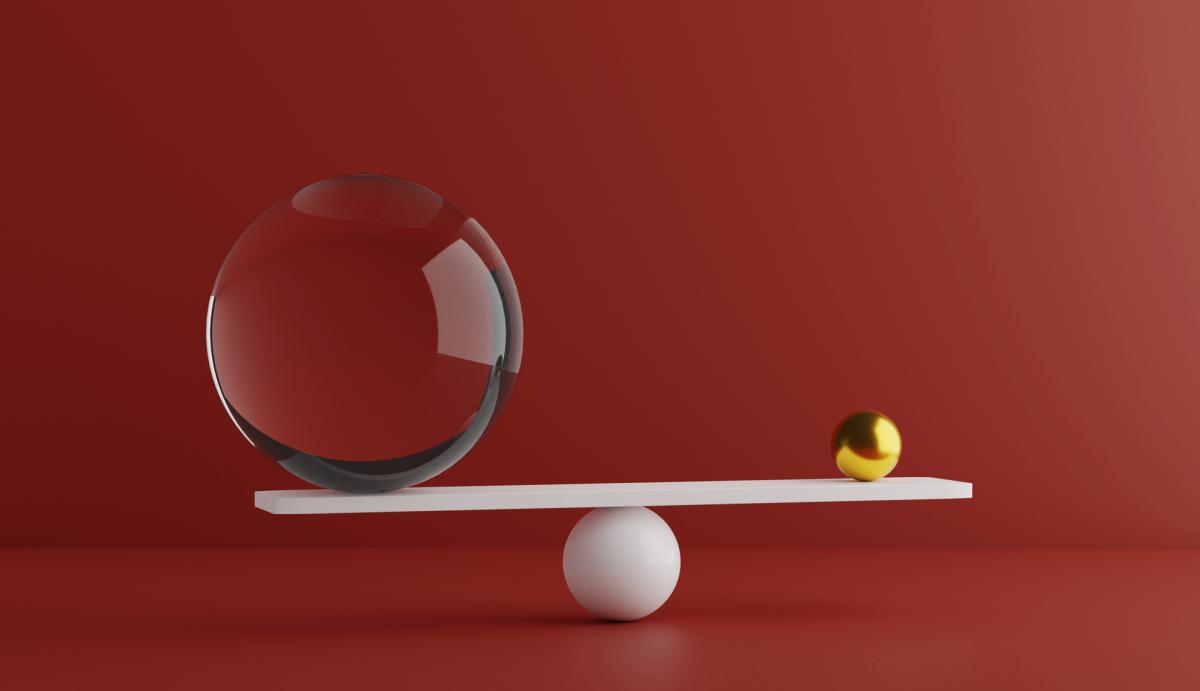

In today’s corporate world, Financial Planning & Analysis (FP&A) plays a critical role in shaping business strategies. Advanced financial models, supported by cutting-edge technology, allow companies to forecast scenarios with increasing levels of precision. However, while accurate predictions are crucial, true success depends on an organisation’s ability to manage businesses with agility and respond swiftly to unforeseen changes.

In this article, I explore how organisations can balance rigorous financial planning with an agile mindset — highlighting the dangers of cognitive biases and offering strategies to prevent reliance on outdated assumptions and past information.

Precise Planning: The Foundation of Strategy

Financial planning accuracy is undoubtedly essential to the success of any business. With the right tools, companies can project detailed financial scenarios and forecast results with a higher degree of certainty than ever. As a global planning director, I had the opportunity to model business performance over 150 times, most notably during our 2021 Initial Public Offering (IPO), where we continuously refined our forecasts, validating assumptions over different time horizons.

However, no matter how precise the financial model, one key insight became clear: even the most accurate forecasts lose their effectiveness if the organisation is not fully committed to executing the strategy and adapting to new realities as they emerge.

The Challenge of Global Strategic Alignment

Working with a global team comes with inherent complexities. During my time leading FP&A in an organisation operating across 18 countries, our biggest challenge was ensuring strategic alignment across diverse regions and business units. Achieving perfect alignment among over 200 global leaders is an exceedingly rare accomplishment.

Yet, despite this challenge, alignment was crucial to our growth. Under this management, the company grew from 2,500 employees to nearly 12,000. However, even with such significant growth, we were impacted by the global tech crisis that emerged in mid-2022. The business could not pivot quickly enough to mitigate the impact, teaching us a valuable lesson about the importance of maintaining agility in management.

The Growth Trap: Overconfidence and Resistance to Change

Our continuous growth over 30 years created a culture of unwavering confidence. Even during periods of deceleration — such as the 2020 pandemic — we had grown accustomed to believing that sales recovery would be swift and inevitable. However, as the FP&A team began presenting scenarios that contradicted the company’s "collective memory," we encountered resistance to new ideas.

Despite our robust financial models and accurate forecasts, the leadership fell into the trap of thinking, "This has never happened before, so it won’t happen now." We ignored early warning signs of a significant market shift, and this lack of flexibility prevented us from acting swiftly to safeguard the business.

Looking back, it’s clear that agility and strategic flexibility could have helped us avoid this trap. By embracing an adaptive mindset rather than relying on assumptions based on past success, we could have recognised emerging risks sooner and taken timely action. Agility isn’t just about reacting to change, it’s about maintaining a readiness to adapt, which is essential for navigating both expected and unexpected shifts.

Strategies to Avoid Biases and Foster Agility

To prevent falling into the trap of past success and to maintain an agile mindset, here are five strategies organisations can implement:

1. Challenge the Status Quo with Pre-Mortem Analysis

A pre-mortem analysis asks teams to envision a future where a project has failed and then work backwards to identify what might have caused it. This approach helps counter overconfidence by encouraging teams to actively consider how their assumptions could go wrong. By focusing on potential failure points, organisations can avoid the "it’s always worked before" mindset.

2. Encourage Cognitive Diversity in Decision-Making

Biases thrive in environments where the same perspectives dominate. To break free from this, it's crucial to foster cognitive diversity in decision-making. Bring in people from different departments, backgrounds and levels of the organisation to inject fresh viewpoints. Diverse thinking challenges groupthink and exposes the organisation to new possibilities, helping it remain agile in the face of change.

3. Create Psychological Safety for Questioning Assumptions

An agile organisation is one where employees feel safe to question existing beliefs. Leaders must cultivate psychological safety, ensuring that individuals can challenge assumptions, raise concerns and propose alternative solutions without fear of negative repercussions. This culture of openness helps teams avoid getting stuck in the bias of overconfidence and makes it easier to respond to new data or market shifts.

4. Use Real-Time Feedback Loops to Counter Bias

Establishing short, frequent feedback loops — as seen in agile methodologies — ensures that decisions are based on current information rather than outdated assumptions. Whether through regular sprint reviews, daily stand-ups or weekly check-ins, these feedback cycles force teams to stay agile and adapt quickly as new data emerges. This helps avoid the trap of sticking to past strategies, which may no longer be relevant.

5. Rotate Leadership on Key Projects to Avoid Entrenched Thinking

Entrenched leadership can lead to rigid thinking and resistance to new ideas. By rotating leadership roles on key projects, organisations can bring fresh perspectives to strategic decisions. This prevents teams from becoming too comfortable with past methods and fosters a culture of continuous innovation and adaptation.

Financial Accuracy and Human Capability

Top-performing FP&A professionals know that financial model accuracy is only part of the equation. Achieving business goals depends on human capability: leaders who can interpret signs of change, adjust their assumptions and make swift, effective decisions. This requires not only technical expertise but also a deep understanding of organisational dynamics and human behaviour.

If, as an FP&A professional, you have yet to develop the ability to align strategies across departments, promote flexible management and challenge established thinking, there is still much room for growth in your journey towards becoming an excellent leader.

Conclusion: Achieving Excellence at the Intersection of Planning and Agility

True excellence in FP&A lies in balancing precise planning with agile business management. No matter how accurate your forecasts are, they mean little if the organisation can’t quickly adjust its strategies to respond to market changes.

Ultimately, it’s people who turn forecasts into reality. A solid financial plan, combined with adaptive leadership, lets organisations not only survive but thrive in uncertain times. In a business world that’s constantly evolving, agility is no longer optional, it’s essential.

As you consider your organisation’s approach, ask yourself: Are your current strategies flexible enough to adapt to changes, or are they overly reliant on past successes? When was the last time your team truly challenged its assumptions, and what did you learn from it? How diverse are the perspectives involved in your decision-making processes, and what fresh insights might you be missing?

By fostering cognitive diversity, promoting continuous reassessment, and building a culture of agility, organisations can avoid relying too much on past successes and stay ready to adapt — whatever the future holds.

The full text is available for registered users. Please register to view the rest of the article.

Related articles

The question many organisations currently have and will have in the future is: “how do we...

How to establish sustainable success in Strategic Finance, one step at a time. When executed correctly...

We’ve all heard the phrase, “Culture Eats Strategy”. This quote often attributed to Peter Drucker is...

As far as I know, we are not legally required to forecast. So why do we...

The benefits of measuring seasonality of accuracy are that users can plan high/low scenarios for each...

+

Subscribe to

FP&A Trends Digest

We will regularly update you on the latest trends and developments in FP&A. Take the opportunity to have articles written by finance thought leaders delivered directly to your inbox; watch compelling webinars; connect with like-minded professionals; and become a part of our global community.