The biggest business issue in the UK is Brexit - and has been since the people’s...

Brexometer for FP&A Professionals: November 2019

November 26, 2019

Beware Friday the thirteenth! Index gets jumpy ahead of the election

Beware Friday the thirteenth! Index gets jumpy ahead of the election

But good economic news pushes Brexometer to the best of the bad

The result of the UK General Election will be known on Friday 13th December, following the polling date of Thursday 12th.

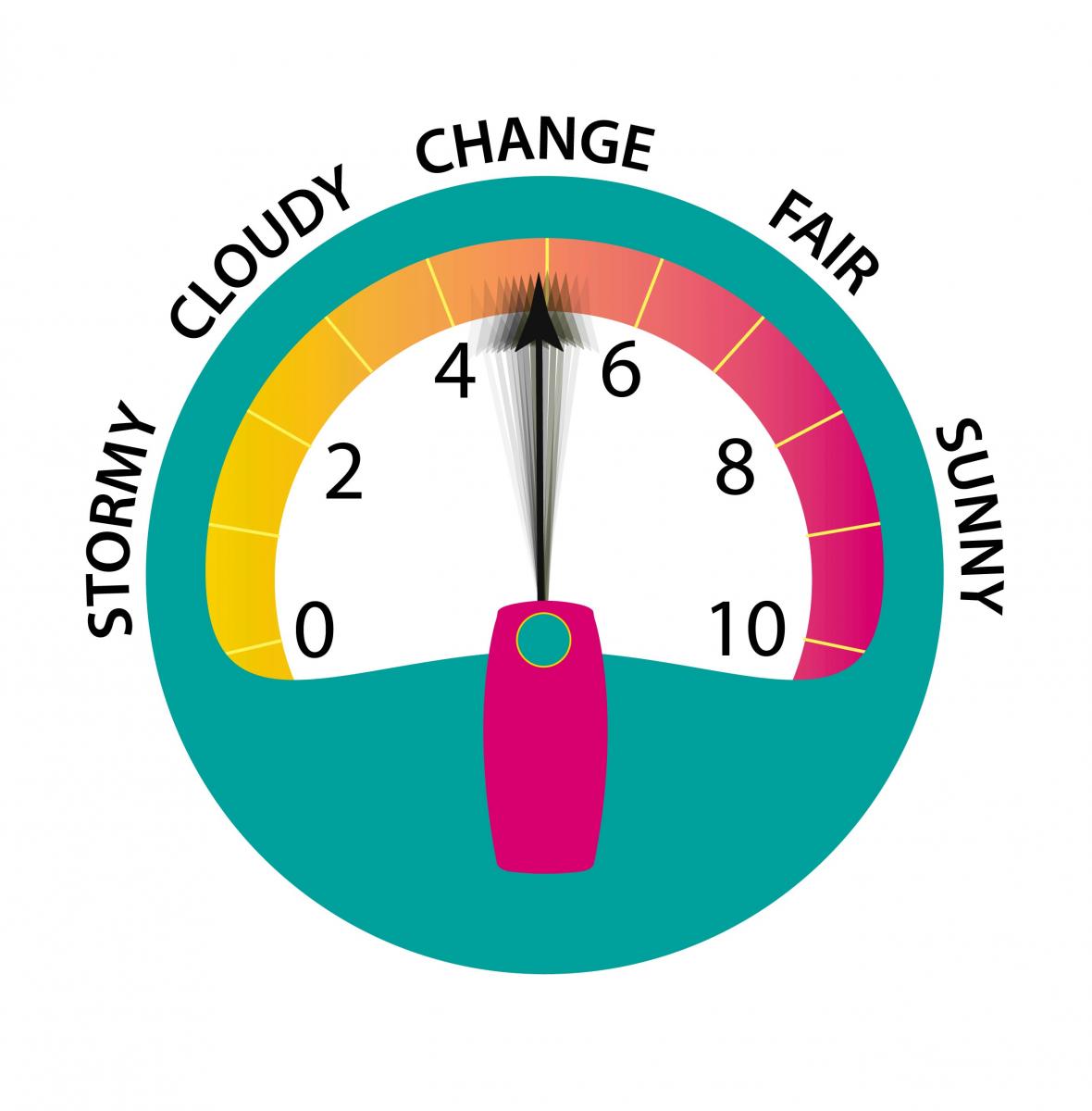

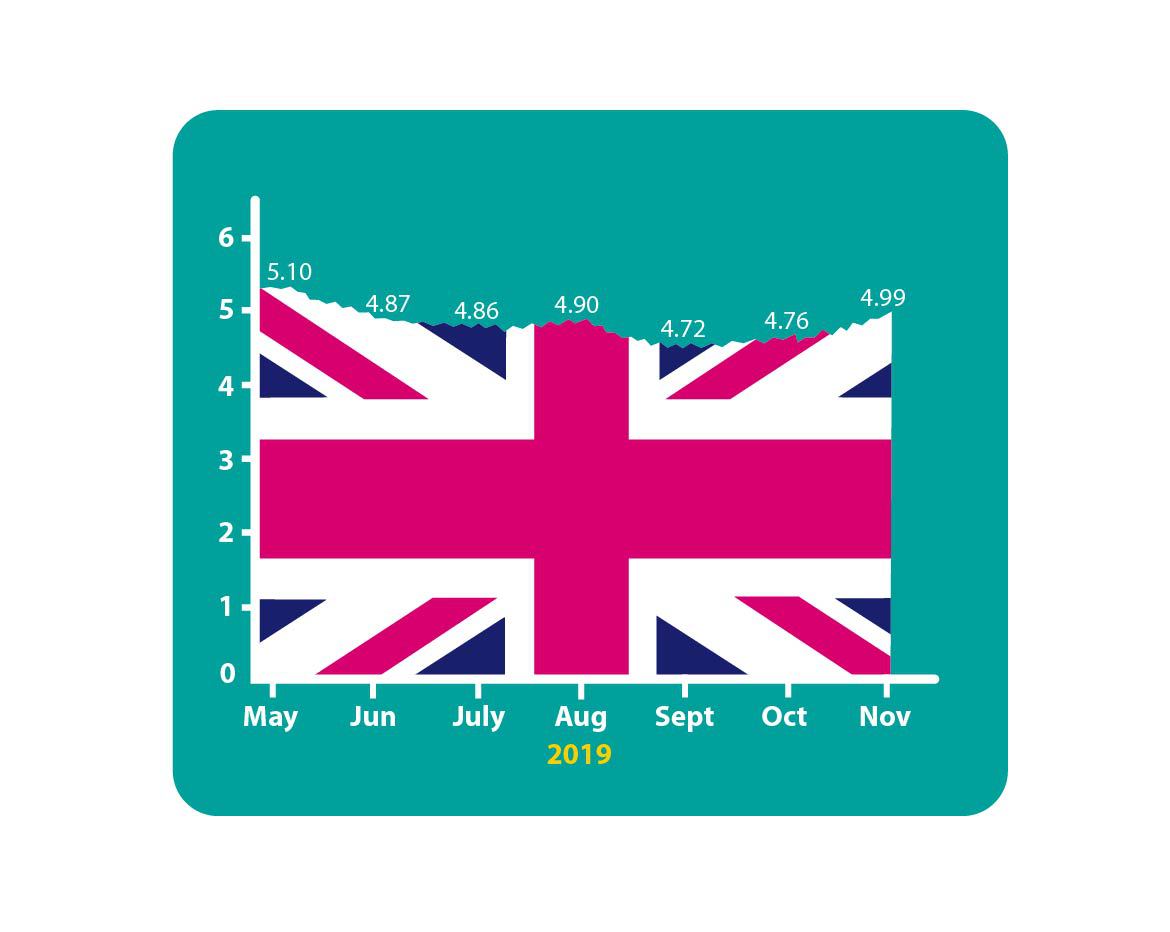

The Accountagility Index (AAX) rose 23 basis points in November to 4.99, from 4.76 in October. The Index records UK political and economic health in a score out of ten. Any score below 5.00 is negative, so we remain in the red rather than in the black this month, but by the slenderest of margins.

What caused the index to go up this month?

There were two highly positive factors at play since last time. 1) The speedy conclusion of the Brexit negotiations between Boris Johnson’s team and Michel Barnier, the EU Chief Negotiator, which removed the worst risk of a no deal exit. 2) The extension offered by the EU until 31st January 2020 has pushed the date backwards, and the temperature of the relationship improved.

Meanwhile sterling rose in relief and so did the FTSE 100. In fact the other key stock market index, the FTSE 250 representing smaller firms, rose by 6% over the past month. Despite being still below the median mark of 50, the PMI Index rose to 48.7, being helped by the Services sector and some re-stocking ahead of the (now deferred) Brexit date of Halloween. We correctly predicted this rise last month. It is unlikely to rise further during this month, since political uncertainty will deter even hardy optimists from investing.

Were there any falling factors?

Very much so. Although the UK economy grew again during Q3, by 0.3%, this is after a shrinkage during the prior Quarter. The performance of the UK over the last 12 months is a net growth in GDP of only 1.0%. Amidst signs of workforce shedding across most industries, the employment figure, so buoyant over past years, fell back slightly. The only bright spots, as far as this area of the economy is concerned, came from reports of hiring from service providers and a tightening of wages in the Services sector generally. The lack of political stability caused by the Election has weighed on the Index too, as one might expect.

What else has been happening?

The Index for economic factors only, rose 22 basis points from 5.56 last month, to 5.78. Could it be heading back towards the all-time peak of 5.93 in April? This rise may be surprising to many, and indeed the longer-term signs remain extremely downbeat, and probably will until the Brexit uncertainty clears.

What happens next?

The next Brexometer measurement will be taken on Friday 13th December, immediately after the result of the General Election is known. It will then be released on Monday 16th December. The starting bell of the campaign has sounded, and already there are many conflicting signs and stories. Will it be a re-run of the EU Referendum, as some are forecasting? Or will be become a stramash of hundreds of topics, policies, assertions, angles and points, difficult to follow and impossible to call? Meanwhile, will the campaign affect the economy? How will the Index react? Keep following the Brexometer to find out.

The Brexometer was calculated on 11 November 2019.

The full text is available for registered users. Please register to view the rest of the article.

Related articles

Whilst Parliament, the Government, the legislature and the EU have been contributing to a feverish few...

+

Subscribe to

FP&A Trends Digest

We will regularly update you on the latest trends and developments in FP&A. Take the opportunity to have articles written by finance thought leaders delivered directly to your inbox; watch compelling webinars; connect with like-minded professionals; and become a part of our global community.