AI in FP&A creates value when earlier analytical signals are connected to governance, ownership, escalation, and...

AI Will Not Solve Weak Forecasting. It Will Reveal It.

July 9, 2026

Why AI-enabled forecasting challenges KPI logic and forces FP&A to earn governance through competence.

Artificial Intelligence is often positioned as a way to improve forecasting. That is true, but it misses the harder point. In many organisations, forecasting does not fail first because the algorithm is weak. It fails because the steering logic is weak: management trusts the wrong signals, FP&A works with an incomplete view of the drivers, and key assumptions are not challenged early enough.

Many forecasts look disciplined from the outside: calendar closed, assumptions collected, numbers consolidated, variances explained. Yet a disciplined process can still rest on weak driver logic. A dashboard can make a weak forecast visible. It cannot make the business logic true. Forecasting still fails when the organisation cannot explain why customers buy less, why churn rises, why margin pressure starts or why cost behaviour changes.

AI will not remove that weakness on its own. Where driver understanding, decision routines or accountability are missing, AI is more likely to expose the gap than to close it. The future of forecasting is therefore not better prediction alone. It is a broader shift from projecting outcomes to understanding drivers, challenging KPIs, intervening earlier and governing the response.

For CFOs, this is the uncomfortable implication. AI-enabled forecasting does not only test model quality; it tests whether management is steering the business through the right drivers. The risk is not only forecast error. It is capital allocated too late or to the wrong place, interventions that come after the signal was already visible, and confidence in KPIs that no longer explain performance.

The Wrong Debate: AI Versus Excel and BI

A familiar forecasting debate asks whether AI will replace Excel, BI or EPM systems. That is not the useful question. Excel still matters for modelling flexibility and commercial judgement. BI and EPM still matter for transparency, standardisation and repeatable reporting. Without these foundations, AI-enabled forecasting may become faster, but not more trustworthy. The more precise issue is the BI gap: governed information does not automatically become governed decision capability. An organisation can see performance clearly and still lack the routines, decision logic and governance structures needed to act on it consistently. This distinction builds on the analytics literature and is central to the BI gap argument (Davenport & Harris, 2007; Chen, Chiang & Storey, 2012; Grover et al., 2018; Seufert, 2026b).

Analytic AI adds a different kind of capability. It can work closer to customers, products, transactions, behaviours and operational drivers. GenAI can help translate these patterns into a management narrative, but the narrative is not the evidence. It still has to be challenged. As systems become more agentic, analytical outputs can be connected to workflow triggers, exception routing and bounded actions. Forecasting governance then shifts from controlling information to controlling decision points: what the system may observe, classify, prepare, escalate or execute, and under which boundaries. This is not a replacement story. It is a capability-expansion story. Each layer increases management potential and governance burden at the same time (Raisch & Krakowski, 2021; NIST, 2023; Seufert, 2026a).

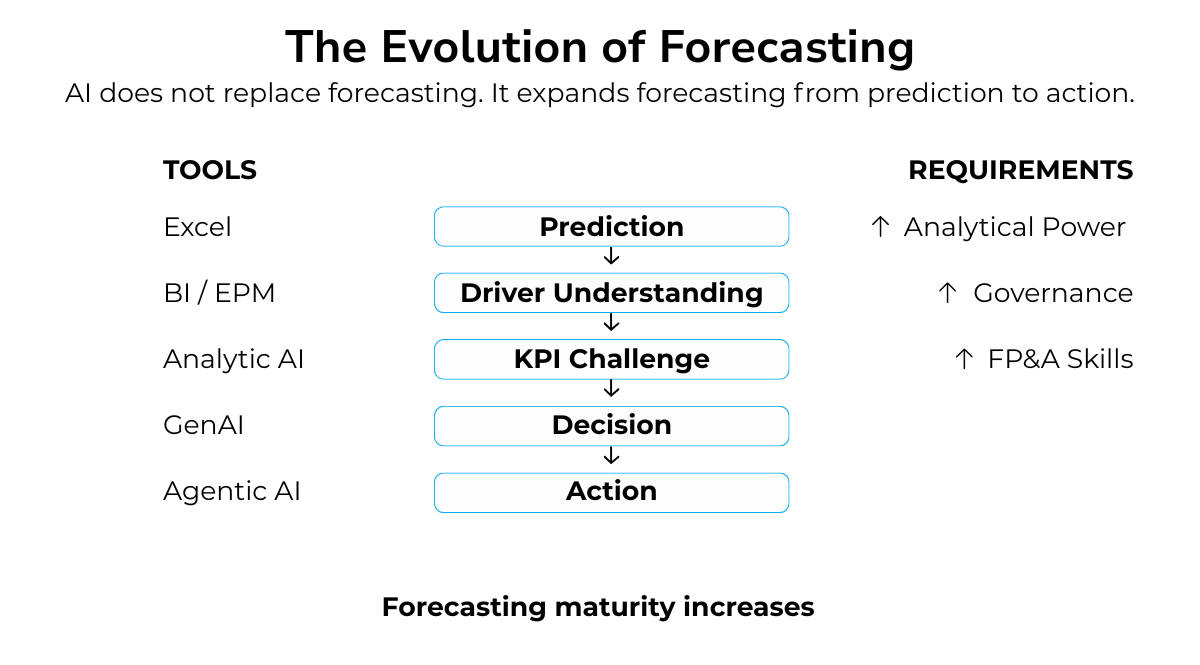

Figure 1 summarises this maturity shift: as forecasting moves from prediction to action, the analytical capability increases, but so do the governance and FP&A skill requirements.

Figure 1

From Prediction to Intervention

Forecasting now has to answer three management questions. What will happen? Excel, BI and EPM help FP&A model outcomes, consolidate assumptions and report likely performance. Why might it happen? Analytic AI can move forecasting from aggregate projection toward driver and behaviour modelling. What should happen next? Prescriptive analytics, GenAI and agentic AI raise the governance bar because signals must be interpreted, escalated and translated into action.

Prediction, explanation and intervention are different management acts. Shmueli's distinction between explaining and predicting is important here: predictive accuracy is not the same as managerial understanding. A model can predict an outcome without explaining the business drivers behind it. A forecast can therefore become more accurate without becoming more useful. Advanced analytics should not be described as a machine that automatically discovers causality. The stronger claim is narrower: AI-enabled forecasting becomes more decision-oriented when predictive models are connected to driver analysis, counterfactual reasoning, domain judgement and explicit decision routines (Shmueli, 2010; Bertsimas & Kallus, 2020; Fernández-Loría & Provost, 2022).

For FP&A, the practical consequence is clear. AI improves forecasting only when prediction is connected to driver logic, decision logic and accountable action. Predictive models can inform prescriptive decisions under uncertainty, but they do not remove the need to separate correlation, explanation and causal decision-making. That separation is where FP&A judgement remains essential (Bertsimas & Kallus, 2020; Fernández-Loría & Provost, 2022).

From Outcome Forecasting to Driver Forecasting

Traditional forecasting often starts with historical aggregates: last year's sales, current run rate, expected growth, budget assumptions, average margin, known pipeline or management overlays. These inputs still matter. The problem is that they often describe the financial outcome more than the business cause. Analytic AI changes the level of analysis.

Instead of only asking how revenue is likely to develop, FP&A can ask which customers are likely to buy, reduce spend, churn or respond to pricing actions. Instead of only forecasting costs at the cost-centre level, FP&A can examine which operational drivers drive cost volatility. Instead of only projecting margin from product mix, FP&A can analyse transaction-level discounting, service intensity, fulfilment patterns or customer profitability.

This is not just a more advanced time-series forecast. It is a different forecasting logic, closer to where outcomes are created. Forecast errors may therefore reveal more than statistical limitations. They may reveal that the organisation does not yet understand the drivers it claims to manage (Shmueli, 2010; Fernández-Loría & Provost, 2022).

The KPI Challenge

For FP&A, the uncomfortable implication is that analytic AI can produce evidence that existing KPIs are incomplete, lagging or only weakly connected to future performance. That is not automatic proof of causality. It is a direct challenge to the organisation's steering logic: which indicators are merely visible, and which indicators help explain what will happen next? (Kaplan & Norton, 1992; Ittner & Larcker, 2003).

A sales forecast may be governed by pipeline value and weighted probability. Customer-level modelling may show that renewal behaviour, usage intensity, pricing sensitivity or service issues provide earlier evidence of revenue risk. A margin forecast may focus on product mix, while transaction-level analysis may point to discount approvals, fulfilment complexity, or service intensity. A cost forecast may follow budget ownership, while operational data points to process exceptions, volume volatility or service-level requirements.

The harder FP&A question is simple: are we forecasting the business correctly if we are not steering it through the right drivers? Analytic AI may not make its most important contribution by improving the forecast number. It may make it by showing that the organisation's steering logic has to be challenged before forecasting can improve. At that point, forecasting becomes a management-control issue rather than a reporting exercise (Kaplan & Norton, 1992; Ittner & Larcker, 2003; Brynjolfsson, Hitt & Kim, 2011).

A Revenue Forecast Example

Consider a revenue forecast that begins to weaken. In a traditional forecast review, the issue often becomes visible only in the monthly cycle. Sales updates the pipeline. FP&A consolidates the view. Management sees a downside risk. The discussion then starts in the familiar place: is Sales too pessimistic, can key deals still close, and should the forecast be adjusted?

Now, assume the pipeline still looks stable. An analytic AI layer detects a different pattern four weeks earlier: product usage in a key customer segment falls by 18%, renewal probability declines, discount dependency rises from 12% to 21%, and service tickets increase among accounts that historically reduce spend after unresolved issues. The forecast risk is not yet obvious in the aggregate revenue number, but customer-level signals are deteriorating.

The conversation changes. The question is no longer only whether the pipeline supports the forecast. The question is whether pipeline value is still the right early-warning KPI for this part of the business. If customer behaviour explains revenue risk before pipeline value, then forecasting has exposed a steering problem.

GenAI can turn the pattern into a management explanation: the affected segment, weakening assumptions, scenarios to review and decisions required. But a plausible narrative is not a validated conclusion. As systems become more agentic, they may request a downside scenario, ask Sales to review accounts, trigger a data-quality check or prepare an escalation note. The forecasting system is no longer only producing a number. It is connecting signals, explanations and responses.

A Margin and Cost Forecast Example

The same governance challenge appears in margin and cost forecasting. A margin forecast may remain stable at the business-unit level while transaction-level analysis reveals increasing discount leakage, fulfilment complexity or service intensity. Reported margin may still be on plan while exception-based discounts rise from 9% to 16% of transactions in one region. A cost forecast may appear under control within budget categories while operational data points to process exceptions, supplier volatility or volume shifts that precede financial effects.

The management question is the same. Are current KPIs identifying the drivers early enough, or are they reporting financial consequences after the underlying behaviour has already changed? AI does not simply improve the forecast. It tests whether FP&A is monitoring the right drivers and governing the right early-warning indicators.

For a forecast review, this shifts the meeting agenda. FP&A should not only ask whether the number is right. It should force five management questions before the forecast is approved:

What FP&A Should Ask in a Forecast Review

Which driver changed before the financial number changed?

Which KPI gave the earliest warning signal?

Is the current forecast logic explaining the business or only extrapolating outcomes?

Who has the authority to challenge the KPI logic?

What management action should follow from the signal?

If these questions cannot be answered, the forecast review has not yet governed the forecast. It has only reviewed the number.

The FP&A Governance Gap

The KPI challenge leads directly to governance. The critical issue is not only who owns the model. It is who has the competence, authority and accountability to understand the signal, challenge the driver logic, document the assumptions, escalate the exception and ensure that management action follows. For CFOs, forecasting therefore moves beyond planning accuracy. It becomes a governance question: who is qualified to decide which signals should shape resource allocation, risk escalation and management action?

IT has a legitimate role in architecture, access, integration and security. Data science has a legitimate role in model design, performance and methodology. Risk and compliance have a legitimate role in controls, auditability and standards. Sales, operations, and business teams have a legitimate role in customer, market, and process actions.

FP&A can be a credible governance candidate because forecasting sits inside the management-control system: financial steering, scenario logic, KPI architecture, resource allocation, performance routines and accountable decisions. But this role is not automatic. FP&A cannot claim governance over AI-enabled forecasting while remaining only a consumer of BI outputs.

This is the FP&A governance gap. BI and dashboards create transparency, but analytics capability requires more than consuming outputs. AI-enabled forecasting requires FP&A to understand how signals are produced, which assumptions shape them, which drivers matter, which KPIs deserve attention and which response should follow. Governance follows competence, not organisational tradition. In decision-governance terms, FP&A must be able to define decision points, autonomy boundaries, tool access, escalation rules, accountability, monitoring and audit evidence before claiming a governance role (Seufert, 2026a; Seufert, 2026b).

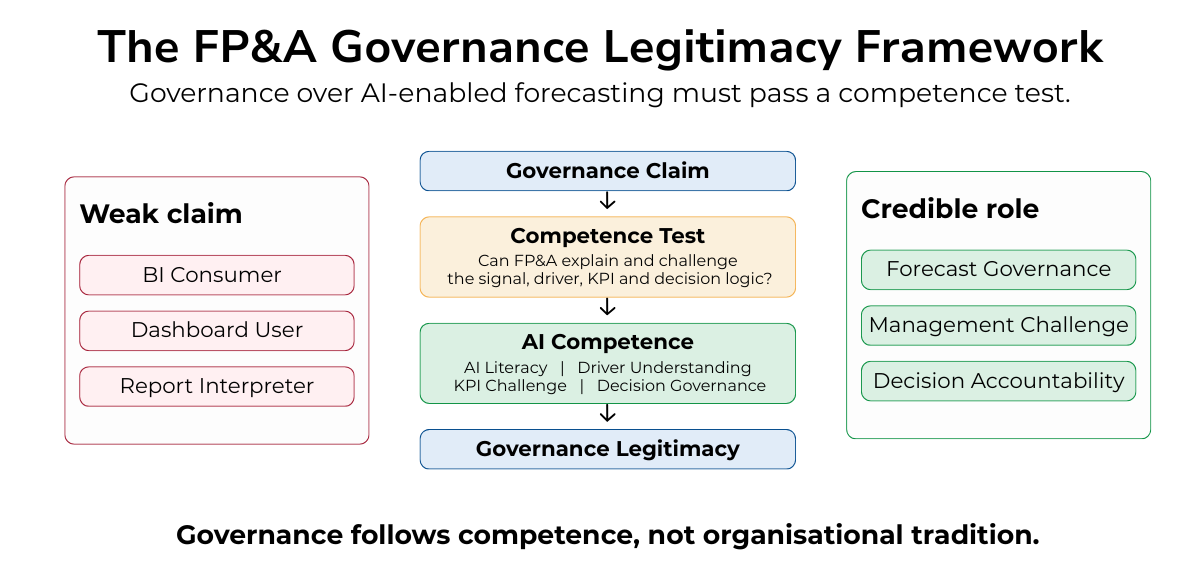

Figure 2 shows the competence test FP&A must pass before it can credibly govern AI-enabled forecasting.

Figure 2

Skills are the Basis of Legitimacy

AI skills in FP&A are therefore not a side topic. They are the basis on which the governance claim becomes credible.

AI skills do not create FP&A's governance role; FP&A's relevance comes from its position in the management-control system. But AI skills legitimise that role in an AI-enabled forecasting environment. NIST's AI Risk Management Framework, ISO/IEC 42001 and the EU AI Act point in the same direction: organisations remain responsible for governing AI systems through risk management, oversight, documentation and accountability mechanisms. Governance cannot simply be delegated to technology. It requires competent human oversight that can understand, challenge, document and escalate model-supported decisions. Human oversight without sufficient competence is not governance (NIST, 2023; ISO/IEC, 2023; European Parliament and Council, 2024; Seufert, 2026a).

In practice, this also makes AI-enabled forecasting a lifecycle discipline. Data quality, model limitations, documentation, monitoring, auditability and technical debt have to be governed across the forecasting system, not treated as implementation details after the model is deployed (Sculley et al., 2015; Amershi et al., 2019; Mitchell et al., 2019; Raji et al., 2020; Gebru et al., 2021).

FP&A does not need to become a data-science function. But it does need business-driver literacy, data and model literacy, KPI architecture, decision governance and executive translation. It must understand model limitations, uncertainty, data quality, driver assumptions, decision boundaries and escalation routines well enough to challenge AI-supported forecasts. A function cannot credibly govern a forecasting system it does not understand.

Forecasting after AI

AI-enabled forecasting creates a strategic choice for FP&A. One option is to remain the function that consolidates numbers, explains variances and manages the planning cycle. That work will still matter, but it will become less distinctive as automation improves.

The stronger option is to govern the management-control logic around forecasting: which drivers matter, which KPIs are valid, which model signals are trusted, which uncertainties are material and which responses should follow. FP&A does not need to own every model. It does need to earn the right to govern the management response that follows from forecast signals.

The future of forecasting is not a better spreadsheet, a richer dashboard or a more automated forecast. It is a management-control system that can predict outcomes, explain drivers, challenge KPI logic and govern responses responsibly. AI-enabled forecasting will not reward the finance function with the most precise forecast. It will reward the function that understands why performance changes, which signals deserve trust and which management actions should follow.

The next challenge for FP&A is no longer whether AI can improve forecasting. The challenge is how forecasting systems should be redesigned when prediction, driver analysis, KPI challenge and management intervention become part of the same governance process.

That question cannot be solved by another dashboard, another model or another planning cycle. It requires a new operating model: decision points, escalation logic, autonomy boundaries, human oversight, accountability and management action. This is where the next article will continue: how FP&A can design the operating model for governed AI-enabled forecasting and decision-making.

References

Amershi, S., Begel, A., Bird, C., DeLine, R., Gall, H., Kamar, E., Nagappan, N., Nushi, B., & Zimmermann, T. (2019). Software engineering for machine learning: A case study. Proceedings of the 41st International Conference on Software Engineering: Software Engineering in Practice.

Bertsimas, D., & Kallus, N. (2020). From predictive to prescriptive analytics. Management Science, 66(3), 1025–1044.

Brynjolfsson, E., Hitt, L. M., & Kim, H. H. (2011). Strength in numbers: How does data-driven decision-making affect firm performance? SSRN Working Paper.

Chen, H., Chiang, R. H. L., & Storey, V. C. (2012). Business intelligence and analytics: From big data to big impact. MIS Quarterly, 36(4), 1165–1188.

Davenport, T. H., & Harris, J. G. (2007). Competing on Analytics: The New Science of Winning. Harvard Business School Press.

European Parliament and Council. (2024). Regulation (EU) 2024/1689 laying down harmonised rules on artificial intelligence (Artificial Intelligence Act). Official Journal of the European Union.

Fernández-Loría, C., & Provost, F. (2022). Causal decision making and causal effect estimation are not the same... and why it matters. INFORMS Journal on Data Science, 1(1), 4–16.

Gebru, T., Morgenstern, J., Vecchione, B., Vaughan, J. W., Wallach, H., Daumé III, H., & Crawford, K. (2021). Datasheets for datasets. Communications of the ACM, 64(12), 86–92.

Grover, V., Chiang, R. H. L., Liang, T.-P., & Zhang, D. (2018). Creating strategic business value from big data analytics: A research framework. Journal of Management Information Systems, 35(2), 388–423.

ISO/IEC. (2023). ISO/IEC 42001:2023 Information technology — Artificial intelligence — Management system.

Mitchell, M., Wu, S., Zaldivar, A., Barnes, P., Vasserman, L., Hutchinson, B., Spitzer, E., Raji, I. D., & Gebru, T. (2019). Model cards for model reporting. Proceedings of the Conference on Fairness, Accountability, and Transparency, 220–229.

National Institute of Standards and Technology. (2023). Artificial Intelligence Risk Management Framework (AI RMF 1.0). NIST AI 100-1.

Raji, I. D., Smart, A., White, R. N., Mitchell, M., Gebru, T., Hutchinson, B., Smith-Loud, J., Theron, D., & Barnes, P. (2020). Closing the AI accountability gap: Defining an end-to-end framework for internal algorithmic auditing. Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, 33–44.

Raisch, S., & Krakowski, S. (2021). Artificial intelligence and management: The automation–augmentation paradox. Academy of Management Review, 46(1), 192–210.

Sculley, D., Holt, G., Golovin, D., Davydov, E., Phillips, T., Ebner, D., Chaudhary, V., Young, M., Crespo, J.-F., & Dennison, D. (2015). Hidden technical debt in machine learning systems. Advances in Neural Information Processing Systems, 28.

Seufert, A. (2026a). Agentic AI in Management Control Systems: A Decision Architecture for Governing AI Agents. SSRN Working Paper.

Seufert, A. (2026b). The BI Gap: From Business Intelligence to Governed AI-enabled Decision Capability. Executive Research Report. SSRN Working Paper.

Shmueli, G. (2010). To explain or to predict? Statistical Science, 25(3), 289–310.

Ittner, C. D., & Larcker, D. F. (2003). Coming up short on nonfinancial performance measurement. Harvard Business Review, 81(11), 88-95.

Kaplan, R. S., & Norton, D. P. (1992). The balanced scorecard: Measures that drive performance. Harvard Business Review, 70(1), 71-79.

The full text is available for registered users. Please register to view the rest of the article.

Related articles

FP&A Agent Managers will become essential as AI agents move from task automation into forecasting, scenario...

In this article, the author explains how AI in FP&A can evolve from automation to a...

In this article, the author examines how FP&A teams can implement trustworthy agentic AI by matching...

How Headless FP&A and Agentic AI are reshaping budgeting through real-time scenario modelling, conversational planning, and...

In this article, the author explains how CFOs can build “AI-ready FP&A” teams through disciplined governance...

+

Subscribe to

FP&A Trends Digest

We will regularly update you on the latest trends and developments in FP&A. Take the opportunity to have articles written by finance thought leaders delivered directly to your inbox; watch compelling webinars; connect with like-minded professionals; and become a part of our global community.