How Headless FP&A and Agentic AI are reshaping budgeting through real-time scenario modelling, conversational planning, and...

AI in FP&A: From Analytical Signals to Management Decisions

July 2, 2026

Why finance teams need to turn Artificial Intelligence into decision capability, not just analytical output.

Many FP&A teams can now generate forecasts, detect anomalies and analyse performance faster than before. Yet the management problem often begins after the signal appears: who trusts it, who challenges it, who owns the response and when should management act?

Forecasts, dashboards, anomaly detection and scenario models can make commercial and financial risks visible earlier. That helps, but it does not automatically change the next pricing discussion, capacity decision, or cash review. In many organisations, the handover from analysis to action remains informal and dependent on routines, relationships and the willingness of business leaders to accept revised assumptions.

The bottleneck is not visibility alone. It is the ability to turn visibility into accountable action.

This changes the central FP&A question. The issue is not only whether AI can improve analysis. In many areas, it already can. The more important question is whether finance can use AI-enabled insight to make management decisions faster and more accountable.

AI rarely fixes a weak decision system. It tends to make weaknesses harder to ignore.

Decision System, Not Tool Category

A decision system is the combination of data, KPI logic, review routines, responsibilities, escalation paths and governance through which financial information becomes management action. It is not a new organisational layer, but the way the organisation already steers performance, made explicit enough to test.

This view is consistent with the management-control perspective that control systems do not merely report performance; they shape attention, challenge assumptions and guide action on strategic priorities (Simons, 1995).

The same signal can lead to different outcomes depending on who owns the review, whether the KPI definition is accepted, whether the issue has a route into an operating forum and whether escalation thresholds are taken seriously.

AI is therefore not the decision system. It is one support mechanism inside it. It can prepare evidence, compare options, highlight exceptions, test assumptions and accelerate scenarios. Whether that improves management control depends on how the output is used.

AI is therefore not the decision system. It is one support mechanism inside it. It can surface signals, prepare evidence, compare options, test assumptions and accelerate scenarios. Whether this improves management control depends on how the output enters review routines, escalation paths and accountable decisions.

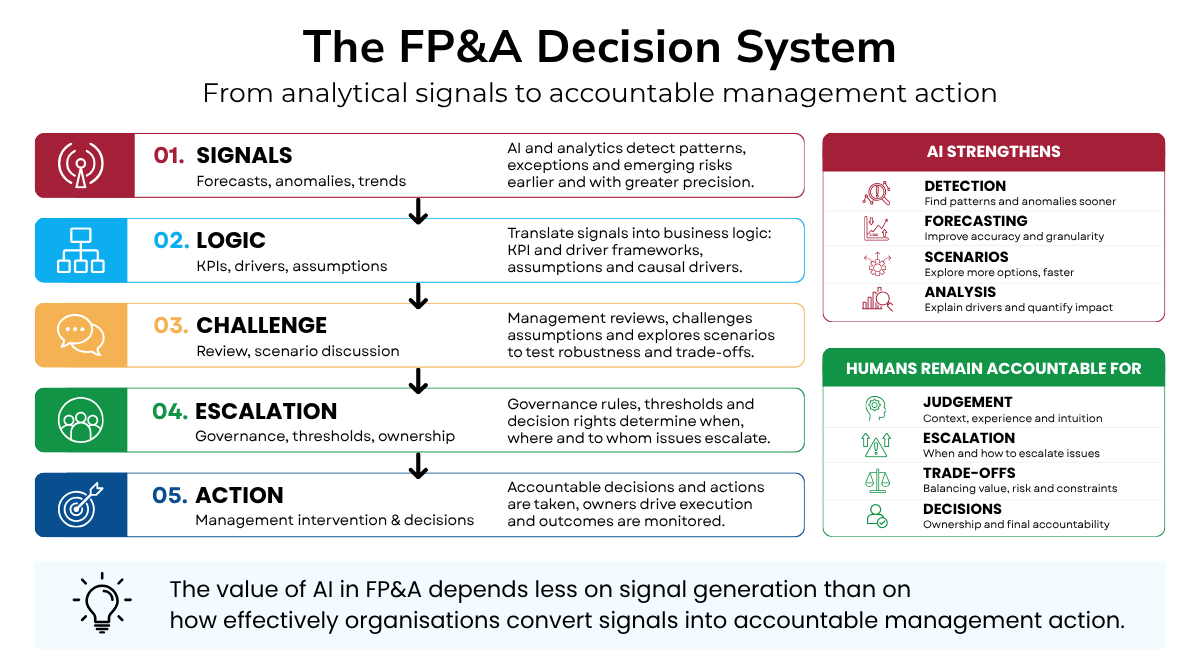

A practical FP&A decision system can be simplified into five stages: signals, logic, challenge, escalation and action. Signals show what is changing. Logic defines interpretation. Challenge tests assumptions and scenarios. Escalation determines when an issue becomes a management priority. Action is where decisions and accountability occur. The model is simple because common FP&A failure points are simple: unclear definitions, weak routines, no owner, no threshold, no follow-up.

AI can strengthen several stages of this system. It can identify signals earlier, support scenarios and prepare better evidence for review. But accountability remains with the people who set thresholds, accept or reject assumptions, make trade-offs and act on the consequences. The framework below illustrates how analytical signals become accountable management action inside an FP&A decision system.

Figure 1. The FP&A Decision System

This becomes more important as AI moves from analytical support towards more agentic participation in management processes. In a related working paper on agentic AI in management control systems, Seufert (2026) argues that the control question changes when AI systems not only generate information, but also observe signals, classify exceptions, trigger workflows, escalate issues or execute bounded actions.

At that point, governance has to be specified at the level of decision points: decision rights, autonomy boundaries, tool access, oversight, accountability, monitoring and auditability. For FP&A, leaders need to define what AI can analyse, where it sits in the decision system, which decision rights it can support, and which forms of human judgment remain required.

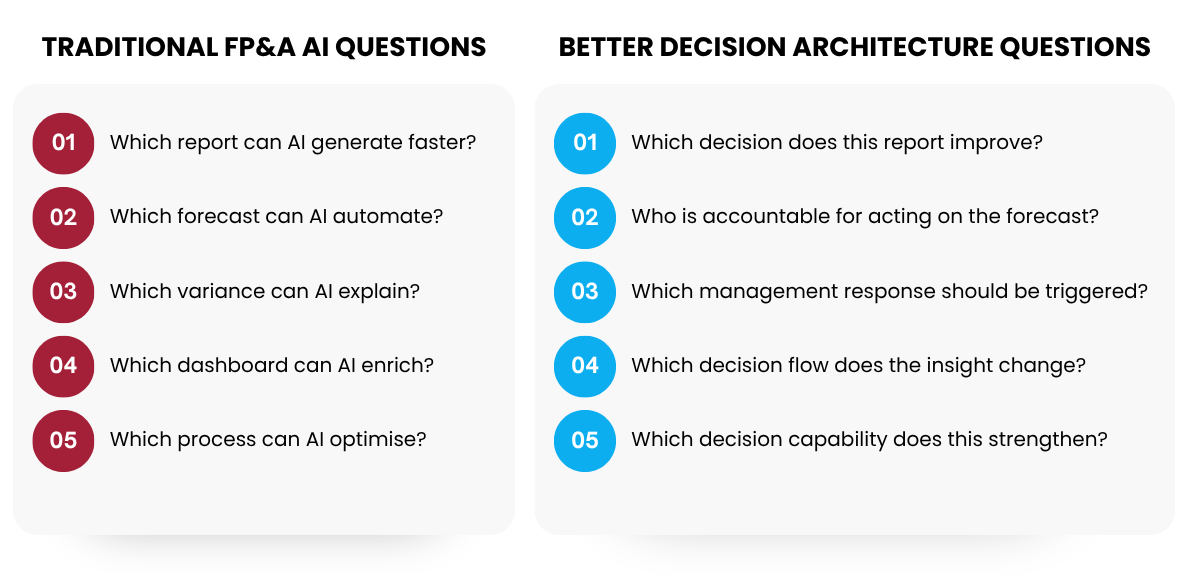

From AI Use Cases To Decision Architecture

Many AI initiatives in FP&A still begin with technology framing: what can be automated, accelerated or enriched? That is reasonable for productivity discussions, but too narrow for management control.

Figure 2: From AI Use Cases to Decision Architecture

A more useful test is whether the AI-enabled output changes a management decision, clarifies accountability or improves response quality. The better question is not only what the tool produces, but what the next management meeting should do differently because of it.

What The Evidence Supports

Evidence increasingly points in the same direction. AI adoption across finance is no longer the primary differentiator. The organisations creating sustained value are those that redesign workflows, governance and decision routines rather than deploying AI as a standalone technology.

Recent surveys support this pattern from different perspectives. KPMG (2026) reports broad AI adoption across finance, together with generally positive business outcomes. McKinsey (2025) finds that leading organisations redesign workflows and strengthen executive AI governance rather than focusing on isolated use cases. BCG (2025) similarly concludes that finance organisations achieve the highest returns when AI is embedded into broader business transformation instead of being treated as a standalone deployment.

The implication for FP&A is straightforward. Competitive advantage does not primarily come from adopting AI. It comes from embedding AI into a governed decision system that connects analytical insight with ownership, escalation and accountable management action.

A technically useful output can still lose value if ownership, decision rights or follow-up routines are unclear.

Why Transparency Is Not Enough

BI and EPM platforms have improved finance. They standardised reporting, professionalised planning processes and made performance information more transparent. That remains important. But transparency and control are not the same thing.

A dashboard can show a margin issue without clarifying whether pricing, sales, operations or finance should act. A forecast can reveal downside risk without defining escalation or ownership. A variance explanation can be accurate and still leave the next decision unchanged.

This is where many use-case discussions become incomplete. They ask whether a task can be automated or accelerated. FP&A leaders should ask whether the task sits inside a decision that management actually owns.

A Practical Test For FP&A Leaders

Before scaling an AI use case, FP&A leaders can apply five checks:

1. Decision objective

Name the management decision first: price changes, margin intervention, liquidity actions, resource allocation, forecast escalation or cost-control measures. If the decision cannot be named, the use case is probably still a productivity idea.

2. KPI and driver logic

Terms such as EBITDA, contribution margin, forecast accuracy, plan variance, product margin and business driver need consistent meaning across functions. Otherwise, better tooling reproduces the inconsistency faster.

3. Workflow integration

The output needs a defined landing point: for example, a weekly forecast review, pricing escalation process, cash committee, sales-performance dialogue or planning cycle. Otherwise, the insight remains an observation. Many pilots lose momentum because the model produces a useful signal, but cadence, ownership and escalation path were not redesigned around it.

4. Governance and judgement

The closer the analytical output gets to management decisions, the clearer validation, accountability, override logic and escalation should be. NIST’s AI Risk Management Framework treats governance, measurement and risk management as part of trustworthy system design, not as an afterthought (NIST, 2023). In FP&A, that means knowing when the tool informs, when a person challenges, who can override the output and who is accountable for the final decision.

5. Roles and capabilities

As routine reporting becomes more automated, FP&A work can shift towards decision partnering, assumption challenge, scenario facilitation and operating-model design. AI ROI then becomes an operating-model question, not only a tooling question.

How This Looks In Practice

In forecasting, an earlier signal about a weakening revenue trend is useful only if the organisation has defined thresholds, ownership and a forum for corrective action.

Consider a forecasting process where AI identifies a weakening sales trend two weeks earlier than the standard monthly review cycle. The challenge is what the organisation has agreed to do next. Does sales ownership shift into a pipeline review? Are downside thresholds linked to escalation? Do operations revise capacity assumptions? Does the CFO require a revised liquidity scenario?

Earlier revenue signals create value only when thresholds, ownership and escalation are already defined. Otherwise, AI produces earlier warnings without improving management control.

In working capital, earlier visibility of overdue receivables, inventory build-up or payment behaviour matters when it connects to credit policy, collection priorities, supply-chain decisions and cash-flow accountability.

In margin management, customer- or product-level margin erosion can be detected before the monthly variance cycle. The value comes when pricing ownership, commercial escalation and profitability trade-offs are explicit enough to change action.

Where Caution Is Needed

Not every FP&A process is ready for more analytical automation. If planning assumptions are politically negotiated, KPI definitions are unstable, data ownership is weak or trust in finance processes is low, additional signals can add noise before they improve control. This is a practical constraint, not an objection to AI.

The point is not to delay AI adoption. It is important to be clear about the conditions under which AI can improve decision quality. Some finance teams will need to stabilise definitions, ownership and review routines before additional automation creates real steering value.

In practice, AI maturity is limited by management-system maturity. The first intervention may be to stabilise definitions, ownership, thresholds, review cadence and escalation logic.

The Maturity Question

Many companies ask how advanced they are with AI. For FP&A, the better question is: which decisions can be supported better, faster and more responsibly than before?

That question gives CFOs and FP&A leaders a diagnostic agenda: Which decisions take too long? Which reports rarely trigger action? Which assumptions are manually stabilised every cycle? Which KPI definitions remain contested? Which decision rights are unclear? Which escalations depend more on relationships than formal routines?

Those questions are less fashionable than a tool roadmap. They are closer to the work that determines whether FP&A improves management control.

Conclusion

AI will be critical for FP&A, but tool adoption alone will not determine its impact on management. Advantage comes when AI is connected to clear data logic, governance, roles and management routines.

A useful maturity test is not simply whether FP&A uses AI. It is whether earlier signals lead to clearer ownership, faster escalation and better decisions in the forums where performance is managed.

Many organisations already generate more analytical insight than management teams can absorb. The harder task is to turn signals into accountable action through stable KPI logic, review routines, escalation mechanisms and clear decision rights.

AI will increasingly become part of the FP&A infrastructure. Its value will depend less on model sophistication than on how effectively organisations connect insight to management action.

For FP&A, the advantage will not come from more signals. It will come from organisations that know what to do when the signal arrives.

Series Note

This article sets out the decision-system logic. The next articles will apply it to forecasting, working-capital steering, margin management, scenario planning and governance. Each will ask whether AI merely creates another signal or improves the route to accountable management action.

References

Boston Consulting Group. (2025, June 4). How to get ROI from AI in the finance function. https://www.bcg.com/publications/2025/how-finance-leaders-can-get-roi-from-ai

KPMG. (2026). Global AI in Finance Report: The Decision Advantage. https://kpmg.com/xx/en/our-insights/ai-and-technology/kpmg-global-ai-in-finance-report.html

McKinsey & Company. (2025, March 12). The state of AI: How organisations are rewiring to capture value. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai-how-organizations-are-rewiring-to-capture-value

National Institute of Standards and Technology. (2023). Artificial intelligence risk management framework (AI RMF 1.0). https://www.nist.gov/itl/ai-risk-management-framework

Seufert, A. (2026, May). Agentic AI in Management Control Systems: A Decision Architecture for Governing AI Agents. SSRN Working Paper / Preprint. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6716098

Simons, R. (1995). Levers of control: How managers use innovative control systems to drive strategic renewal. Harvard Business School Press.

The full text is available for registered users. Please register to view the rest of the article.

Related articles

In this article, the author introduces a governed AI decision architecture that helps FP&A teams generate...

In this article, the author explains why agentic AI adoption in FP&A depends less on technology...

In this article, the author examines how FP&A teams can implement trustworthy agentic AI by matching...

In this article, the author explores how AI-driven tools are shifting FP&A from manual processes to...

In this article, the authors show how AI agents can turn messy earnings call transcripts into...

+

Subscribe to

FP&A Trends Digest

We will regularly update you on the latest trends and developments in FP&A. Take the opportunity to have articles written by finance thought leaders delivered directly to your inbox; watch compelling webinars; connect with like-minded professionals; and become a part of our global community.